The Economists lied

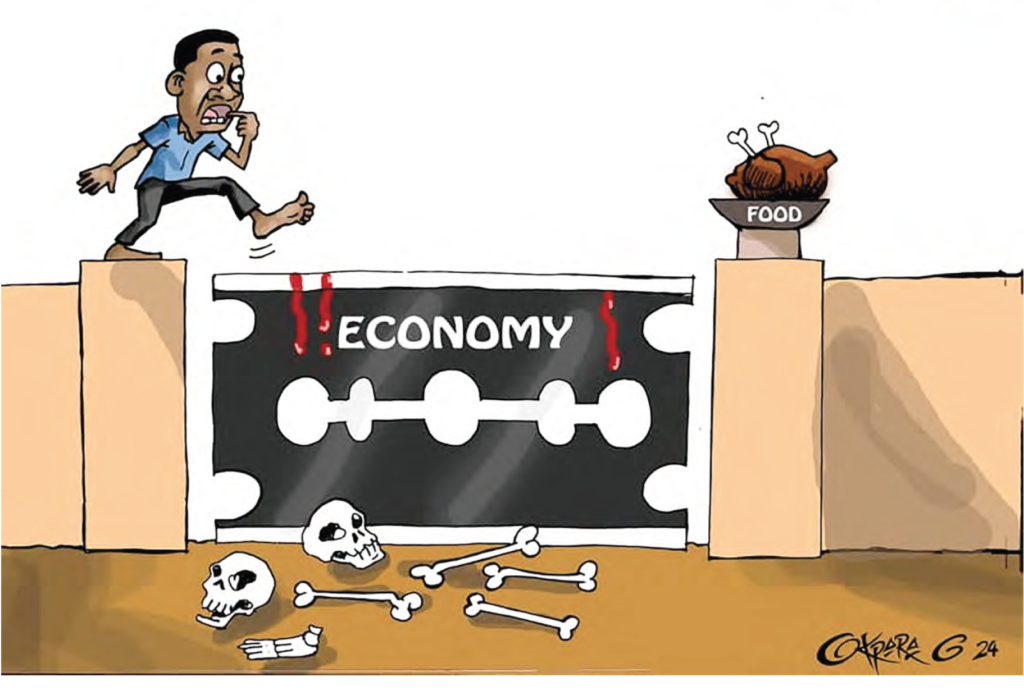

The Economists lied In concluding his seminal treatise on, “The General theory of Employment, Interest and Money,” John Marynard Keynes submitted that “—- the ideas of economists and political philosophers both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed, the world is ruled by little less. Practical men, who believe themselves to be exempt from any intellectual influences are usually the slaves of some defunct economist. Madmen in authority who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back. I am sure that the power of vested interests is vastly exaggerated compared to with the gradual encroachment of ideas. Not indeed, immediately but after a certain interval, for in the field of economic and political philosophy, there are not many who are influenced by new theories after they are twenty-five and thirty years of age, so that the ideas which civil servants and politicians and even agitators apply to current events are not likely to be the newest. But soon or late, it is ideas not vested interests which are dangerous for good or evil” Before May 29th, 2023, there were heated formal and informal debates about the trouble with the Nigerian economy. Many economists and policy analysts attributed the problem to the huge funds paid out as fuel subsidies and the multiple exchange rates which allocated the scarce foreign exchange in a non transparent manner, in some cases, to non-economic operators. These two policies turned a few privileged individuals and politicians with no visible economic activities to billionaires overnight. They believed that only the rich benefited from the fuel subsidy. There was also the feeling that fuel was cheapest in Nigeria and that encouraged smuggling and black-market racketing in neighbouring countries which did not help the economy. The singsong was that the fuel subsidy drained the economy of the resources that would have been channeled to develop it and prosper the people. The belief was that the proceeds from the removal of fuel subsidy will be invested in infrastructure development, agriculture for food security, social welfare and human capital development such as healthcare, skill acquisitions, education as well as security of lives and properties. The air was ridden with calls for the removal of the fuel subsidy. In that frenzy, everybody became an economist, analyzing, pontificating and recommending how our economy will become an Eldorado for everybody if fuel subsidy is removed and multi-exchange rate is harmonized. Many of these economists believe that all subsidies are inherently bad and unless the subsidies are removed, Nigeria will not have a robust economy. The voice of the pseudo-economists drowned that of the real economists. In our country, once a profession or calling becomes fashionable and trendy, everybody wants to be so addressed. Economics is an influential profession that gives one the leverage to express an opinion on the direction of the economy and social life. People want to be addressed as Economists. Our journalists who are supposed to know better, do not help matters, as they address every public opinion analyst as an Economist. Finally, the call for the removal of the fuel subsidy was answered by President Bola Ahmed Tinubu on 29th May, 2023 when in his inaugural address, he declared that, “Fuel Subsidy is gone”. The President later confessed that the transformative statement, “subsidy is gone” was not part of the original text of his inaugural address which he was reading. On his instinct, he extemporaneously declared it in the middle of his speech and it became a policy of his government. The implication is that his transition committee and his economic think-tank committee may not have evaluated it as a priority takeoff policy to include in the inaugural address. Probably, they deferred it for later appraisal and implementation. Where then did the President get the confidence to announce such a far-reaching policy. It must have been from the clarion calls for it by Economists, public policy analysts, pseudo-economists, multilateral financial institutions, the work done by his transition team and the fact that the previous administration did not budget for the payment of subsidies beyond June, 2023. Even if the previous administration did not budget for fuel subsidies beyond June, 2023, the President on inauguration could have presented a supplementary budget for fuel subsidies. Before, May 29, 2023, fuel sold at N165 per litre. On the announcement of fuel subsidy removal and its implementation by NNPC, the fuel price shot up to N589 per litre. In November, 2025, fuel sold at N930. When the epic fury war between the United States and Israel on one side and Iran on the other side started on February, 28th 2026, the fuel price jumped to N1,300 per litre. On the Exchange rate harmonization policy, the Federal Government through the Central Bank of Nigeria merged the multiple exchange rates to align with the parallel market. This was done on June 14th, 2023. By June, 13th, 2023, the official rate was N471/$ and the parallel rate was N765/$ which gave a difference of N287/$. On the merger of the rates on June, 14th,2023, a devaluation of 31%occurred and the official rate moved to N620/$ and the parallel market was N765/$. By 15th June, 2023, the official rate graduated to N657/$ and the parallel inched to N791/$. Sometime in 2024, the rate went haywire as low as N1,900/$ until the CBN intervened by restructuring the foreign exchange market with forex reforms, cancelled the license of many bureau de change, commenced funding the market using the BDCs in the market. It is true that money has been saved by the removal of the fuel subsidy. The removal has boosted government finances. On the other hand, it has greatly impoverished Nigerians. The Federation Accounts Allocation Committee (FAAC) has shared more revenues to the States and Local Government Areas. In 2023, the FAAC allocation to States was N3.58trillion. This rose to N5.81Trilion in 2024 which amounted to 61.6% increase